This printed article is located at http://hongfok.listedcompany.com/financials.html

Financials

Condensed Interim Financial Statements For The Six Months and Full Year Ended 31 December 2025

Financials Archive![]() Note: Files are in Adobe (PDF) format.

Note: Files are in Adobe (PDF) format.

Please download the free Adobe Acrobat Reader to view these documents.

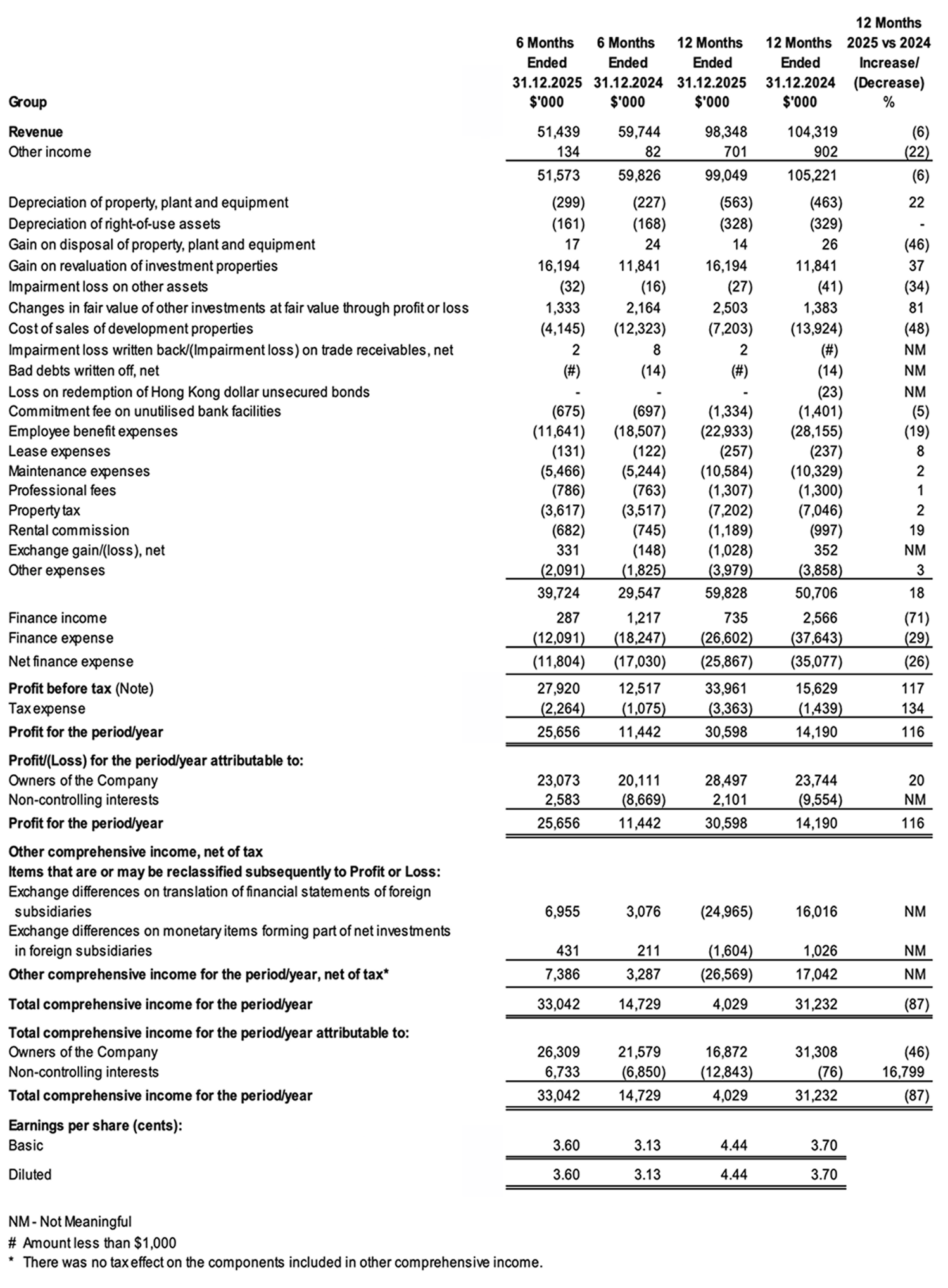

Condensed Interim Consolidated Statement Of Comprehensive Income

Note:

Included in Profit before tax is profit on sale of development properties of approximately $1,537,000 and $3,674,000

(2024: $4,931,000 and $5,540,000) respectively for the six months and full year ended 31 December 2025.

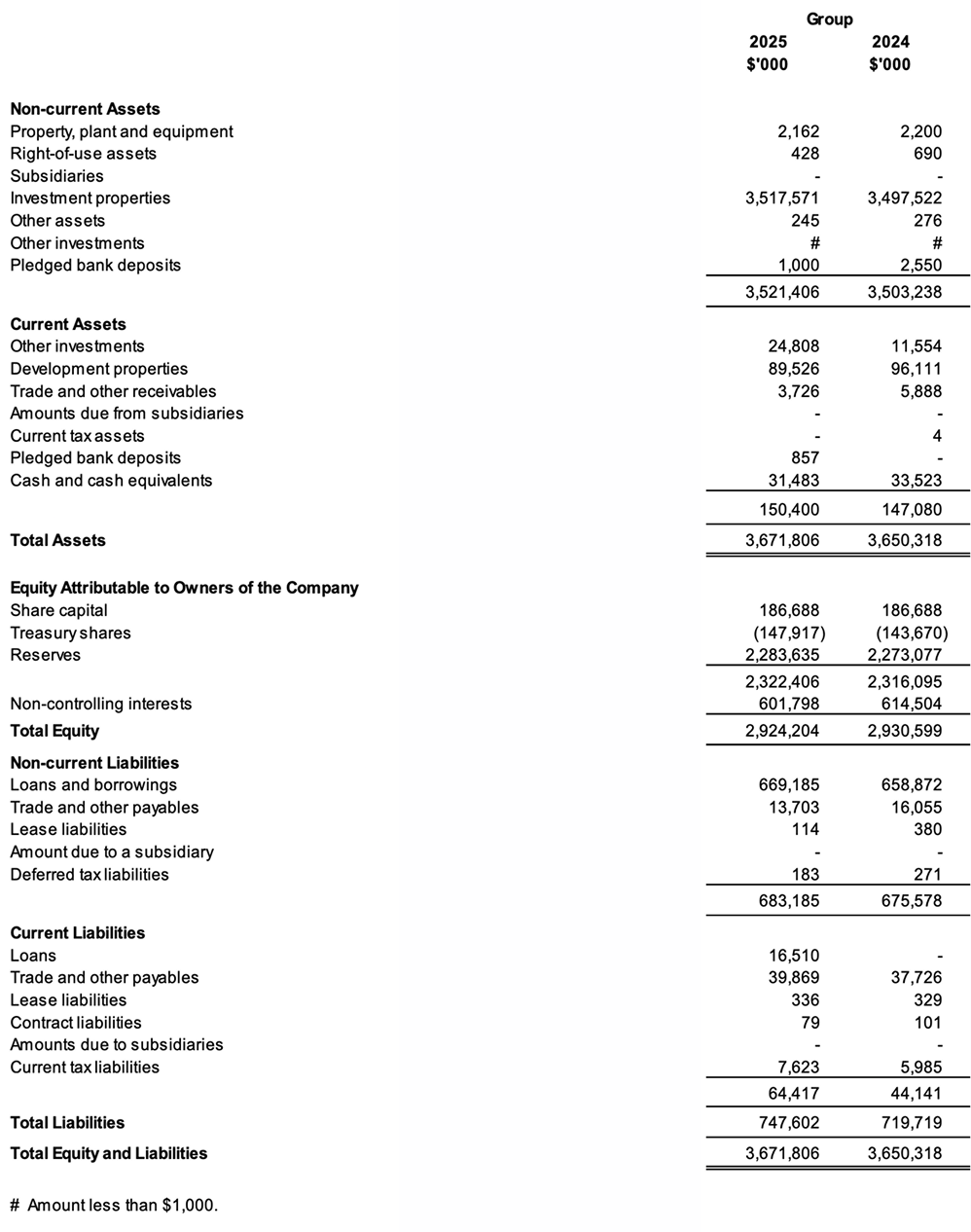

Condensed Interim Statements Of Financial Position

Review of Performance

The Group posted a revenue of approximately $98.3 million for 2025 as compared to approximately $104.3 million for 2024. The decrease in revenue of approximately $6.0 million was mainly due to decrease in the sale of its residential units in Concourse Skyline but this was partially offset by higher rental income from its investment properties.

The Group's other income decreased mainly due to the one-off gain on redemption of its debt investments in 2024. However, this was cushioned by a one-off income from the completion of the sale of a remnant plot of land at University Road in Singapore.

The increase in depreciation expense arose mainly from the additions of property, plant, and equipment in 2025.

The Group recorded a gain of approximately $16.2 million in 2025 as compared to approximately $11.8 million in 2024 on the revaluation of its investment properties based on independent external valuations as at 31 December 2025.

The changes in fair value of other investments at fair value through profit or loss was mainly due to the net fair value gain in the valuation of its other investments as at 31 December 2025 and higher gain on its disposal of other investments in 2025 as compared to 2024.

With the recognition of lower sales revenue from its development properties, there was also a decrease in cost of sales of development properties.

The decrease in employee benefit expenses was mainly due to less bonus and lower provision for other long-term employee benefits for 2025 as compared to 2024.

The increase in rental commission was due to more new leases of its properties being introduced by real estate agents in 2025 as compared to 2024.

The net exchange loss for 2025 as compared to the net exchange gain for 2024 was due to the strengthening of the Singapore dollar for its investments in securities and cash and cash equivalents denominated in Hong Kong dollar.

The decrease in finance income was mainly due to the absence of the deferred day one gain on Hong Kong dollar unsecured bonds and lower interest rates from deposits placed with financial institutions in Hong Kong.

The decrease in finance expense was mainly due to lower interest rates on its secured loans.

The increase in tax expense was mainly due to higher taxable profit contributions from companies in a tax-paying status.

Overall, the Group posted a profit of approximately $30.6 million in 2025 as compared to approximately $14.2 million in 2024.

Consequently, the Group's profit attributable to Owners of the Company was approximately $28.5 million in 2025 as compared to $23.7 million in 2024.

The decrease in right-of-use assets was mainly due to the depreciation.

The decrease in other assets was mainly due to impairment loss in 2025 for club memberships.

The decrease in pledged bank deposits was mainly due to the prepayment of certain secured loan in 2025.

The increase in other investments was mainly due to the purchase of equity investments and net fair value gain on revaluation of its other investments as at 31 December 2025.

The decrease in development properties was mainly due to the sales of the residential units in Concourse Skyline.

The net decrease in trade and other receivables was mainly due the reclassification of deposits and stamp duties paid in 2024 for the acquisition of five units in International Building to investment properties in 2025. This reclassification was done because the purchase was completed in 2025 and the Group now owns all the units in International Building.

The net increase in total loans and borrowings in 2025 was mainly used for the purchase of units in International Building and the purchase of other investments.

The Hong Kong dollar secured bank loans have been reclassified from non-current liabilities in 2024 to current liabilities in 2025. These loans are due in the third quarter of 2026 and are expected to be refinanced before their maturity dates.

The decrease in lease liabilities was mainly due to the monthly payments of lease commitments.

The increase in current tax liabilities was mainly due to the higher provision of income tax for 2025 as compared to 2024.

Commentary On Current Year Prospects

For the Group’s hotel, YOTEL Singapore Orchard Road, the Group will work towards achieving higher-quality revenue through market segmentation discipline, protecting margins through cost control, strengthening workforce stability and enhancing asset quality and guest experience. The Group remains cautiously optimistic about the general hotel outlook for 2026 and is committed to adapt dynamically to prevailing market conditions.

The Singapore office market in 2026 is expected to remain resilient despite persistent macroeconomic and political uncertainties. The occupancy rate for office units is likely to improve with a return-to-office trend, with office attendance on a gradual climb towards pre-pandemic levels. The rental income for the Group's investment properties is likely to remain stable.

With the prospects for a lower interest-rate environment, the Group is expected to continue recognising revenue from the sale of its residential units in Concourse Skyline.